A Debt Payoff Calculator is an online financial planning tool that calculates the repayment schedule for outstanding debt. It estimates the monthly payment required to eliminate debt within a chosen period or determines how many months are needed to become debt-free based on your current payment amount. Additionally, it calculates the remaining balance after a specific number of payments and the total interest paid throughout the loan term. Because it uses standard amortization formulas, the calculator produces reliable estimates suitable for budgeting, financial planning, and debt management. Financial advisors, lenders, and consumers widely use these calculations to evaluate repayment strategies and compare borrowing costs.

How the Debt Payoff Calculator Works

The calculator begins by collecting essential financial information, including the current debt balance, annual interest rate, monthly payment, and desired payoff period if applicable. It then converts the annual interest rate into a monthly rate before applying amortization formulas to calculate repayment details. Depending on the information entered, the calculator determines the required monthly payment, the total number of payments, remaining balances over time, and the overall interest cost. Furthermore, if you enter an additional monthly payment, the calculator recalculates the repayment schedule and shows how much time and interest you can save. This allows borrowers to compare multiple repayment scenarios before making financial decisions.

Debt Payoff Calculator Formula

Formula

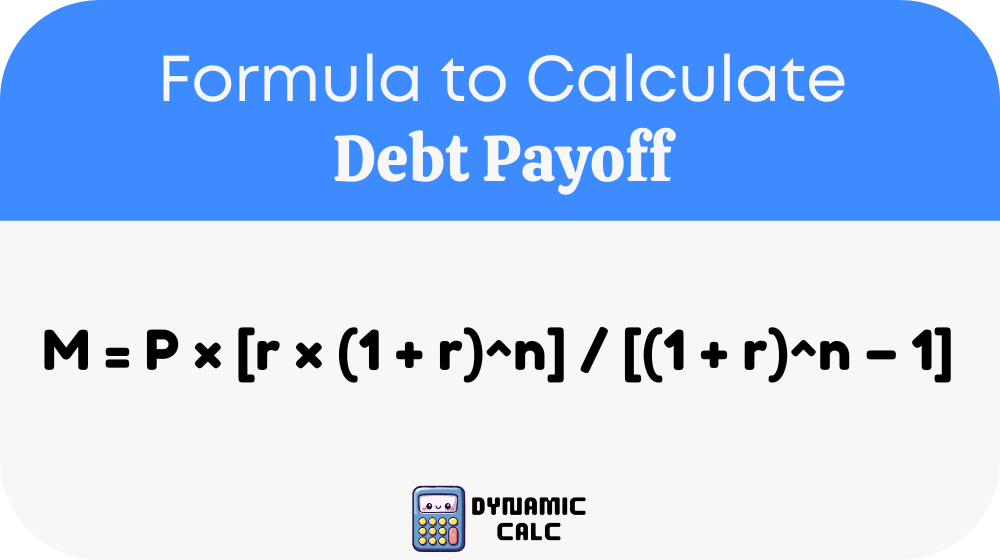

Monthly Payment Formula (for known payoff period):

Where:

- M = monthly payment amount

- P = principal debt balance (initial amount)

- r = monthly interest rate (annual interest rate ÷ 12 ÷ 100)

- n = total number of monthly payments

Number of Payments Formula (for known monthly payment):

n = log(M / (M − P × r)) / log(1 + r)

Where:

- n = number of months required to pay off the debt

- M = fixed monthly payment (must be greater than P × r)

- P = current principal balance

- r = monthly interest rate

Remaining Balance After k Payments:

B_k = P × [(1 + r)^n − (1 + r)^k] / [(1 + r)^n − 1]

Where:

- B_k = remaining balance after k payments

- P = original principal balance

- r = monthly interest rate

- n = total number of payments

- k = number of completed payments

Total Interest Paid:

I = (M × n) − P

Where:

- I = total interest paid

- M = monthly payment

- n = total number of payments

- P = original debt balance

With Extra Payments:

Replace M with (M + E)

Where:

- E = extra principal payment added every month

The calculator then recalculates the number of payments using the Number of Payments Formula, resulting in a shorter repayment period and lower total interest.

Debt Payoff Reference Table

| Debt Type | Typical Repayment Period | Common Interest Rate | Recommended Strategy |

|---|---|---|---|

| Credit Card | 1–10 years | 15%–30% | Pay more than the minimum payment |

| Personal Loan | 2–7 years | 6%–36% | Fixed monthly payments |

| Auto Loan | 3–7 years | 3%–12% | Make extra principal payments |

| Student Loan | 10–25 years | 3%–9% | Income-based or fixed repayment |

| Mortgage | 15–30 years | 4%–8% | Biweekly or additional monthly payments |

| Medical Debt | Varies | 0%–15% | Negotiate payment plans |

| Business Loan | 1–20 years | 5%–15% | Maintain consistent repayment schedule |

Common Financial Conversions

| Annual Interest Rate | Monthly Interest Rate |

|---|---|

| 3% | 0.25% |

| 4% | 0.3333% |

| 5% | 0.4167% |

| 6% | 0.50% |

| 7% | 0.5833% |

| 8% | 0.6667% |

| 10% | 0.8333% |

| 12% | 1.00% |

| 15% | 1.25% |

| 18% | 1.50% |

| 24% | 2.00% |

Example

Suppose you have a debt balance of $15,000, an annual interest rate of 8%, and a monthly payment of $350. The calculator first converts the annual interest rate into a monthly rate by dividing it by 12 and then by 100. It then applies the standard amortization formulas to determine how many months are required to eliminate the debt. After performing the calculations, it estimates the total repayment period, total interest paid, and remaining balance after each payment. If you increase your monthly payment by an additional $100, the calculator recalculates the repayment schedule, demonstrating how the debt can be paid off sooner while significantly reducing total interest costs.

Applications

Credit Card Debt Management

Credit card balances often carry high interest rates, making them expensive when only minimum payments are made. A Debt Payoff Calculator helps borrowers estimate how increasing monthly payments reduces interest costs and shortens the repayment period. It also allows users to compare multiple payment strategies before choosing the most affordable option.

Personal, Auto, and Student Loans

Borrowers can use the calculator to evaluate repayment schedules for installment loans. It estimates monthly payments, total interest, and remaining balances throughout the loan term. Consequently, borrowers gain a better understanding of their financial obligations and can determine whether refinancing or making extra payments would reduce overall borrowing costs.

Financial Planning and Budgeting

Financial planners, households, and businesses use debt payoff calculations to create long-term budgets and debt reduction strategies. By estimating future liabilities, borrowers can allocate income more effectively, prioritize high-interest debt, and improve long-term financial stability. The calculator also supports responsible borrowing decisions before taking on additional debt.

Most Common FAQs

What is a Debt Payoff Calculator?

A Debt Payoff Calculator is a financial calculator that estimates how long it will take to eliminate debt based on the outstanding balance, interest rate, and monthly payment. It also calculates total interest, remaining balances, and the impact of making additional monthly payments. Because it relies on standard amortization formulas, the results provide dependable estimates for personal financial planning, budgeting, and comparing different repayment strategies.

How accurate is a Debt Payoff Calculator?

The calculator is highly accurate when users provide correct loan information and the loan follows a fixed interest rate with regular monthly payments. However, actual repayment may vary if interest rates change, additional fees apply, payments are missed, or lenders modify loan terms. Therefore, borrowers should verify loan details with their lender before making major financial decisions.

Can extra monthly payments reduce interest?

Yes. Extra monthly payments reduce the outstanding principal balance more quickly. As the principal decreases, less interest accumulates over time. Consequently, borrowers often pay off their loans months or even years earlier while significantly reducing total interest expenses. Many financial experts recommend making consistent additional principal payments whenever possible to minimize borrowing costs.