A car loan calculator is a digital finance tool designed to calculate vehicle loan payments based on loan amount, interest rate, loan term, and down payment. This calculator belongs to the financial and automotive loan calculator category. It estimates how much a borrower must pay every month throughout the repayment period. Additionally, it shows the total interest paid and the complete repayment cost over the life of the loan. Financial institutions, dealerships, and personal finance websites commonly provide these calculators to help consumers evaluate financing options. Because auto loans significantly affect long-term budgeting, the calculator serves as an important resource for comparing loan offers and determining whether a vehicle purchase fits within financial limits.

Detailed Explanations of the Calculator’s Working

A car loan calculator works by applying a standard amortization formula that spreads the loan repayment across equal monthly installments. First, the user enters the vehicle price, down payment, loan term, annual interest rate, taxes, and additional fees if applicable. Next, the calculator subtracts the down payment from the total car cost to determine the principal loan amount. Afterward, it converts the annual interest rate into a monthly rate and calculates the number of total monthly payments. Using these values, the calculator determines the fixed monthly installment required to repay both principal and interest. Furthermore, many advanced calculators display amortization schedules, total interest paid, and payoff timelines, helping users understand the long-term financial impact of the auto loan.

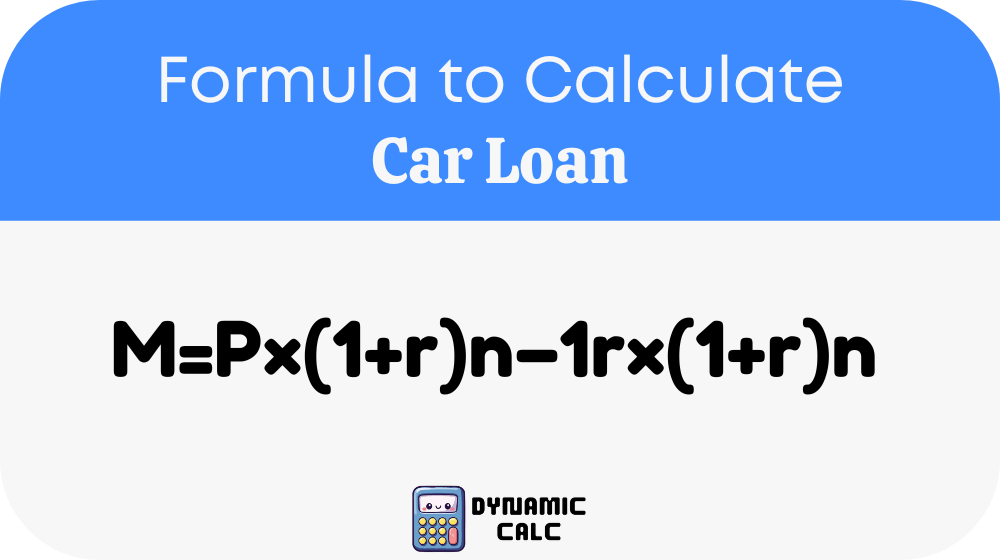

Formula with Variables Description

Where:

- M = Monthly loan payment

- P = Principal loan amount

- r = Monthly interest rate

- n = Total number of monthly payments

- (1 + r)^n = Compound interest factor over the loan period

Variable Details

| Variable | Meaning | Description |

|---|---|---|

| M | Monthly Payment | Fixed amount paid every month |

| P | Principal | Total borrowed amount after down payment |

| r | Monthly Interest Rate | Annual rate divided by 12 |

| n | Loan Duration | Total repayment months |

Interest Rate Conversion Formula

Monthly Interest Rate = Annual Interest Rate ÷ 12 ÷ 100

Common Car Loan Payment Estimates Table

| Vehicle Price | Down Payment | Interest Rate | Loan Term | Estimated Monthly Payment |

|---|---|---|---|---|

| $20,000 | $2,000 | 5% | 5 Years | $339 |

| $25,000 | $5,000 | 6% | 5 Years | $387 |

| $30,000 | $3,000 | 7% | 6 Years | $460 |

| $35,000 | $7,000 | 5.5% | 6 Years | $458 |

| $40,000 | $8,000 | 4.5% | 5 Years | $596 |

| $50,000 | $10,000 | 6.5% | 7 Years | $597 |

General Auto Loan Interest Rate Guide

| Credit Score Range | Estimated APR |

|---|---|

| 750+ | 3% – 5% |

| 700–749 | 5% – 7% |

| 650–699 | 7% – 10% |

| 600–649 | 10% – 15% |

| Below 600 | 15%+ |

Example

Suppose a buyer wants to purchase a vehicle worth $30,000 and makes a $5,000 down payment. The remaining loan amount becomes $25,000. The lender offers an annual interest rate of 6% for a 5-year loan term.

Step 1: Convert annual interest rate into monthly interest rate.

Monthly Interest Rate = 6 ÷ 12 ÷ 100

Monthly Interest Rate = 0.005

Step 2: Determine total number of payments.

5 years × 12 months = 60 payments

Step 3: Apply the formula.

The estimated monthly payment becomes approximately $483.

Step 4: Calculate total repayment.

$483 × 60 = $28,980

Total Interest Paid = $28,980 − $25,000

Total Interest Paid = $3,980

Therefore, the borrower pays approximately $483 monthly over five years.

Applications

Car loan calculators serve multiple financial and automotive financing purposes. They improve borrowing transparency and help users compare financing offers effectively. In addition, they support long-term budgeting and responsible financial planning. Buyers often use these calculators before visiting dealerships to determine affordable payment ranges. Financial institutions also rely on similar calculations when evaluating borrower repayment capability. Furthermore, refinancing applicants use the calculator to estimate potential savings from lower interest rates. Since vehicle purchases involve large financial commitments, accurate payment estimation reduces financial uncertainty and improves confidence during negotiations.

Budget Planning

A car loan calculator helps individuals determine whether a vehicle fits within their monthly income and financial obligations. As a result, buyers can avoid overextending their budgets and reduce the risk of missed payments.

Loan Comparison

Borrowers can compare multiple financing offers by adjusting loan terms, interest rates, and down payments. Consequently, they can identify the most cost-effective financing option available.

Refinancing Evaluation

Vehicle owners use the calculator to estimate refinancing benefits. Lower interest rates or shorter repayment terms may significantly reduce overall borrowing costs and repayment duration.

Most Common FAQs

What is the main purpose of a car loan calculator?

A car loan calculator helps borrowers estimate monthly vehicle payments and total loan costs before applying for financing. It simplifies loan planning by calculating repayment amounts based on interest rate, loan term, and principal amount. Additionally, it allows users to compare different financing options quickly and accurately. Since vehicle purchases often involve long-term financial obligations, the calculator improves budgeting and supports informed decision-making. Many buyers use it to determine affordability and negotiate better financing terms with dealerships or lenders.

How accurate is a car loan calculator?

A car loan calculator provides highly accurate estimates when users enter correct loan details. However, the final payment may vary slightly because lenders can include taxes, registration fees, insurance, processing charges, or additional financing costs. Moreover, credit score changes and lender-specific policies may affect the approved interest rate. Despite these variables, the calculator remains a reliable financial planning tool for estimating monthly installments and total repayment obligations. Therefore, borrowers should use updated financial information for the most realistic calculations.

Does a larger down payment reduce monthly payments?

Yes, a larger down payment directly reduces the principal loan amount, which lowers monthly payments and decreases total interest costs. When borrowers pay more upfront, lenders finance a smaller balance, resulting in reduced financial risk and lower repayment obligations. Additionally, higher down payments may improve loan approval chances and secure better interest rates. Many financial experts recommend making a substantial down payment whenever possible because it minimizes long-term borrowing expenses and reduces the likelihood of negative vehicle equity.