A Bret Whissel Amortization Calculator is an online financial tool that calculates periodic loan payments and generates a complete amortization schedule. The calculator determines how much of each payment goes toward interest and how much reduces the principal balance over time. In addition, it estimates total interest costs, remaining balances, and payoff timelines. Most users apply this calculator to fixed-rate mortgages, auto loans, refinancing plans, and business financing. Unlike simple loan calculators, amortization calculators provide detailed repayment breakdowns for every payment period. Consequently, users gain a clearer understanding of debt reduction and long-term borrowing costs. Financial professionals often rely on amortization schedules to evaluate affordability and repayment efficiency.

Detailed Explanations of the Calculator's Working

The Bret Whissel Amortization Calculator works by applying standard loan amortization formulas to determine equal periodic payments over a fixed loan term. First, the user enters the loan principal, annual interest rate, payment frequency, and repayment duration. Next, the calculator converts the annual rate into a periodic interest rate. It then calculates the fixed payment amount required to fully repay the loan by the end of the term.

Afterward, the calculator generates an amortization schedule showing each payment period separately. Every payment includes two components: interest and principal. Initially, interest consumes a larger portion of the payment because the outstanding balance remains high. However, as the balance decreases, principal repayment increases gradually. Therefore, users can monitor loan progress and identify opportunities for refinancing or early payoff strategies.

Formula with Variables Description

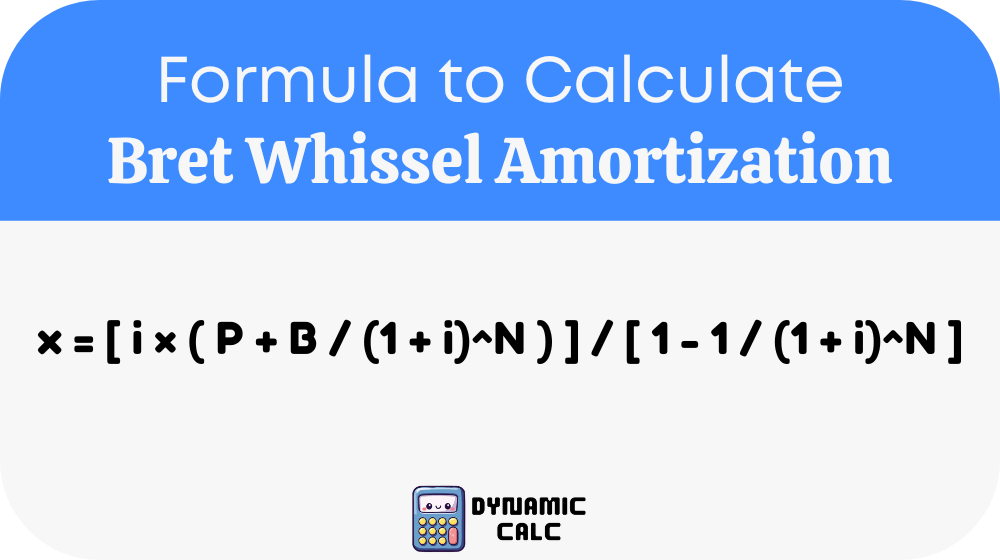

The Bret Whissel Amortization Calculator commonly uses the following amortization payment formula:

Where:

- x = Periodic payment amount

- i = Interest rate per payment period

- P = Principal loan amount

- B = Balloon payment amount or remaining balance

- N = Total number of payment periods

- (1 + i)^N = Compound interest growth factor

This formula helps calculate the exact periodic payment necessary to amortize a loan over a specified timeframe while considering interest accumulation and optional balloon balances.

Common Loan and Mortgage Reference Table

| Loan Amount | Interest Rate | Loan Term | Estimated Monthly Payment |

|---|---|---|---|

| $50,000 | 5% | 10 Years | $530 |

| $100,000 | 6% | 15 Years | $844 |

| $150,000 | 5.5% | 20 Years | $1,032 |

| $200,000 | 7% | 30 Years | $1,331 |

| $250,000 | 6.5% | 30 Years | $1,580 |

| $300,000 | 5% | 30 Years | $1,610 |

| $400,000 | 6% | 30 Years | $2,398 |

| $500,000 | 7% | 30 Years | $3,327 |

Additional Helpful Financial Conversions

| Conversion Type | Formula |

|---|---|

| Annual Interest to Monthly | Annual Rate ÷ 12 |

| Biweekly Payments per Year | 26 Payments |

| Monthly Payments per Year | 12 Payments |

| Loan-to-Income Ratio | Monthly Debt ÷ Monthly Income |

| Total Interest Paid | Total Payments − Principal |

Example

Suppose a borrower takes a $250,000 mortgage loan with a 6% annual interest rate for 30 years. The monthly interest rate becomes:

6% ÷ 12 = 0.5% per month

The total number of monthly payments equals:

30 × 12 = 360 payments

Using the amortization formula, the estimated monthly payment becomes approximately $1,499. During the first payment, a larger portion covers interest charges while a smaller portion reduces the principal balance. However, after several years, the interest portion declines steadily and the principal repayment increases. Consequently, the borrower builds equity faster over time. This example demonstrates how amortization schedules provide transparency regarding long-term loan repayment structures and borrowing costs.

Applications

Mortgage Planning

Homebuyers frequently use amortization calculators to estimate monthly mortgage payments before purchasing property. The calculator helps determine affordability and compare different loan options. Furthermore, borrowers can analyze how varying interest rates affect total repayment costs.

Loan Refinancing Analysis

Borrowers often refinance loans to secure lower interest rates or shorter repayment terms. An amortization calculator helps compare existing loans with refinancing alternatives. Therefore, users can identify potential savings and evaluate whether refinancing benefits outweigh associated costs.

Debt Reduction Strategy

Financial planners use amortization schedules to create effective debt repayment strategies. Users can test extra payment scenarios and determine how additional principal payments reduce interest expenses. As a result, borrowers can shorten loan terms and improve financial stability more efficiently.

Most Common FAQs

What is the purpose of the Bret Whissel Amortization Calculator?

The Bret Whissel Amortization Calculator helps users calculate loan repayment schedules with precision. It determines periodic payments, interest costs, and principal reduction throughout the loan term. In addition, it generates a detailed amortization table that shows how each payment affects the remaining balance. Borrowers commonly use this financial calculator category for mortgages, personal loans, refinancing plans, and auto financing. Because it simplifies complex financial calculations, users can make better borrowing and budgeting decisions confidently.

How accurate is an amortization calculator?

An amortization calculator provides highly accurate estimates when users enter correct loan details. The calculator follows standard financial formulas used by banks, lenders, and mortgage institutions worldwide. However, actual loan costs may differ slightly because of taxes, insurance premiums, lender fees, or variable interest rates. Even so, the calculator remains extremely reliable for estimating monthly payments, total interest, and payoff timelines. Consequently, financial professionals often rely on amortization schedules for planning and analysis purposes.

Can this calculator help reduce loan interest costs?

Yes, the calculator can help borrowers reduce long-term interest expenses. By testing extra payment amounts or shorter loan terms, users can identify strategies that lower total borrowing costs. For example, adding small monthly principal payments often shortens repayment periods significantly. Additionally, refinancing comparisons may reveal opportunities for lower interest rates. Therefore, borrowers can make informed decisions that improve financial efficiency and reduce debt faster over time.